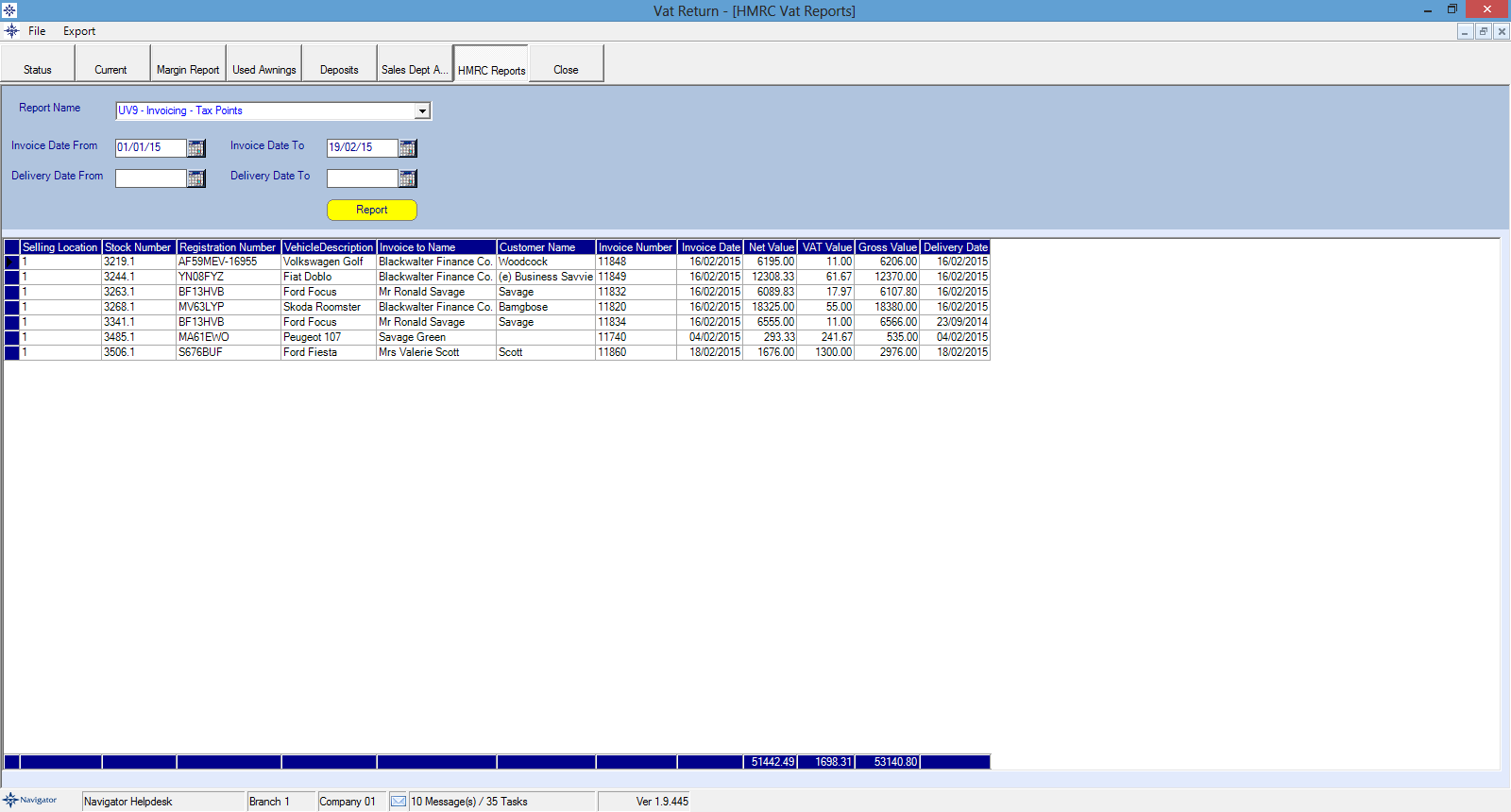

Purpose of Report:

To identify deals where the "14-day" rule for tax points may have been exceeded, and vehicles invoiced in the current VAT period should have been accounted for in the previous period.

Associated Risks:

Section 6(5) of the VAT Act 1994 allows for the creation of a tax point by the issue of a VAT invoice within a period of 14 days after the basic tax point (i.e. the delivery date). Where no invoice has been issued within this period the tax point reverts to the basic tax point. More details can be found in VAT Notice 700 Section 14.2.

Bear In Mind:

•The receipt of a payment in advance of the invoice creates a tax point. Where payment was received in advance of the invoice date the business may have accounted for VAT on it anyway, for example as part of a period end manual adjustment.